For example, as of September 2018, the Federal Deposit Insurance Corporation (FDIC) said that sweeps to bank deposit accounts held $1.7 trillion. As of July 2019, the U.S. Securities and Exchange Commission (SEC) reported that $3.7 trillion was invested in money market funds, another common sweep program investment option.

What are the benefits? And the risks?

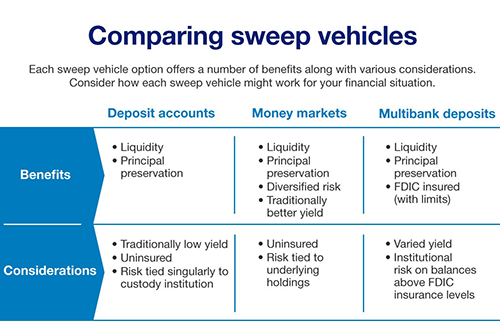

A sweep program offers three key features:

- Liquidity – An investor can seamlessly move funds in and out of the sweep investment whenever they need to.

- Principal preservation – A reliable return of principal is paramount for sweep programs.

- Yield – As with other asset classes, the sweep program investment should offer some level of return.

Part of a custody account opening process includes designating where a customer wants their cash to reside when it’s not otherwise invested. Some custodians’ sweep programs offer multiple options, others provide as few as one. Once the paperwork is processed, cash is swept in and out of the designated investment as needed.

“What really makes the sweep program unique is that an investor only has to give the investment direction once, and that direction is followed every business day,” Markarian said.

Markarian says when an investor asks for cash to remain uninvested, it generally stems from a regulatory or investment policy matter. An investor could also elect to manage the cash investment on their own, but this requires constant account monitoring, quick decisions based on how much cash is available to invest, and executing trades before market close.

“That’s a burdensome amount of administrative work, and you could also incur a commission or trade fee every day depending on who you use for custody,” he said.

As with any investment, there’s some risk in sweep programs, largely tied to the risks of the underlying investments – an important consideration in money market funds. When using a bank deposit account as a sweep vehicle investment, invested funds are generally covered by FDIC insurance up to the first $250,000 in balances per bank, for each bank in which the customer has funds deposited.

“It’s impossible to find a truly riskless investment, but for decades now, sweep vehicle investments have been among the closest to a riskless investment you can find,” Markarian said.

It helps that regulators enhanced the safety net around money market funds after the multibillion-dollar Reserve Fund failed to maintain the $1 price during the financial market turmoil of 2008. In that instance, the share price dropped to 97 cents. Although it represented only the second time the $1 threshold had been broken, the SEC stepped in with a raft of rules to protect investors.

Which sweep vehicle is best for you?

Custodians generally offer 3 sweep options:

1. An interest-bearing deposit with the custodian is the simplest type of sweep vehicle. The custodian records the funds on its books and pays a negotiated yield. Funds placed in deposits at banks may be covered by FDIC insurance up to applicable limits.

2. A money market fund is operated by a third party and its risk is tied to the investments it holds. Money market funds are securities and thus not covered by FDIC insurance. A prime obligation fund invests in corporate debt, a government obligation fund invests in short term U.S. Government debt and a Treasury obligation fund invests in U.S. Treasury debt. In general, money market accounts offer the best yields among sweep vehicle options.

3. A multibank deposit may offer relatively better-or-worse than average yields, yet it is designed to maximize FDIC insurance protection by linking a number of banks within the offering. Therefore, as soon as a deposit nears the $250,000 threshold, the excess balance is shifted to another bank to take advantage of that bank’s $250,000 FDIC limit, and so on. Most programs offer the opportunity for FDIC insurance up to $2.5 million.

Another consideration between the three types of sweep vehicle investments is the daily cutoff time, which is a function of its liquidity. An investment that shuts down activity before 4 p.m. ET could cause problems if you tend to complete your investment activities nearer to the close of the major stock exchanges. “Each option has its own pros and cons, and if you have the ability to choose from among different investments, you view it as you would any investment decision,” Markarian said.

Liquidity Plus

According to Markarian, U.S. Bank considered all of investors’ pain points with existing cash management options in the development of its sweep vehicle, Liquidity Plus. “We’ve sought to solve as many of the problems as we can and basically create one sweep platform that could meet every investor’s needs.”

While offering a late-afternoon cutoff for optimal liquidity, FDIC insurance up to $2.5 million and a targeted yield more in line with money market funds, Liquidity Plus goes a step further with larger deposits.

$2.5 million in FDIC insurance is usually sufficient coverage for most daily sweep balances, but there are times it isn’t. “It’s not uncommon for larger private wealth and institutional accounts to carry average balances in excess of $2.5 million,” said Markarian. “But even smaller accounts can run into issues with a $2.5 million cap – maybe due to bulk investment liquidations, multiple maturities or simply a waiting period between the receipt of a large deposit and its ultimate investment.”

The result can be significant exposure if an investor isn’t diligent. As an example, take an account that has a balance of $4 million. The account uses a multi-bank sweep vehicle with a $2.5 million cap. This means, on any given day, the account likely has at least $1.5 million uninsured by FDIC – which carries the default risk of whatever bank their program administrator uses for overflow balances.

To mitigate such risk, Liquidity Plus doesn’t use bank deposits for balances above the program limit. It simply invests any funds above the $2.5 million level into a government money market fund.

“You should never have to worry about waking up, hearing that a bank failed, and wondering how to deal with a credit exposure that you didn’t anticipate,” Markarian says. “With Liquidity Plus, we provide the opportunity for investors to always have their excess cash in an FDIC insured bank or a money market fund.

With a stable financial history and strong balance sheet, U.S. Bank is an experienced provider of investment services. Our team of professionals can help you find the cash solutions best fit to your organization’s needs. Learn more about Liquidity Plus and your sweep vehicle options by visiting our website or connecting with our team.