Capitalize on today’s evolving market dynamics.

With markets in flux, now is a good time to meet with a wealth advisor.

Key takeaways

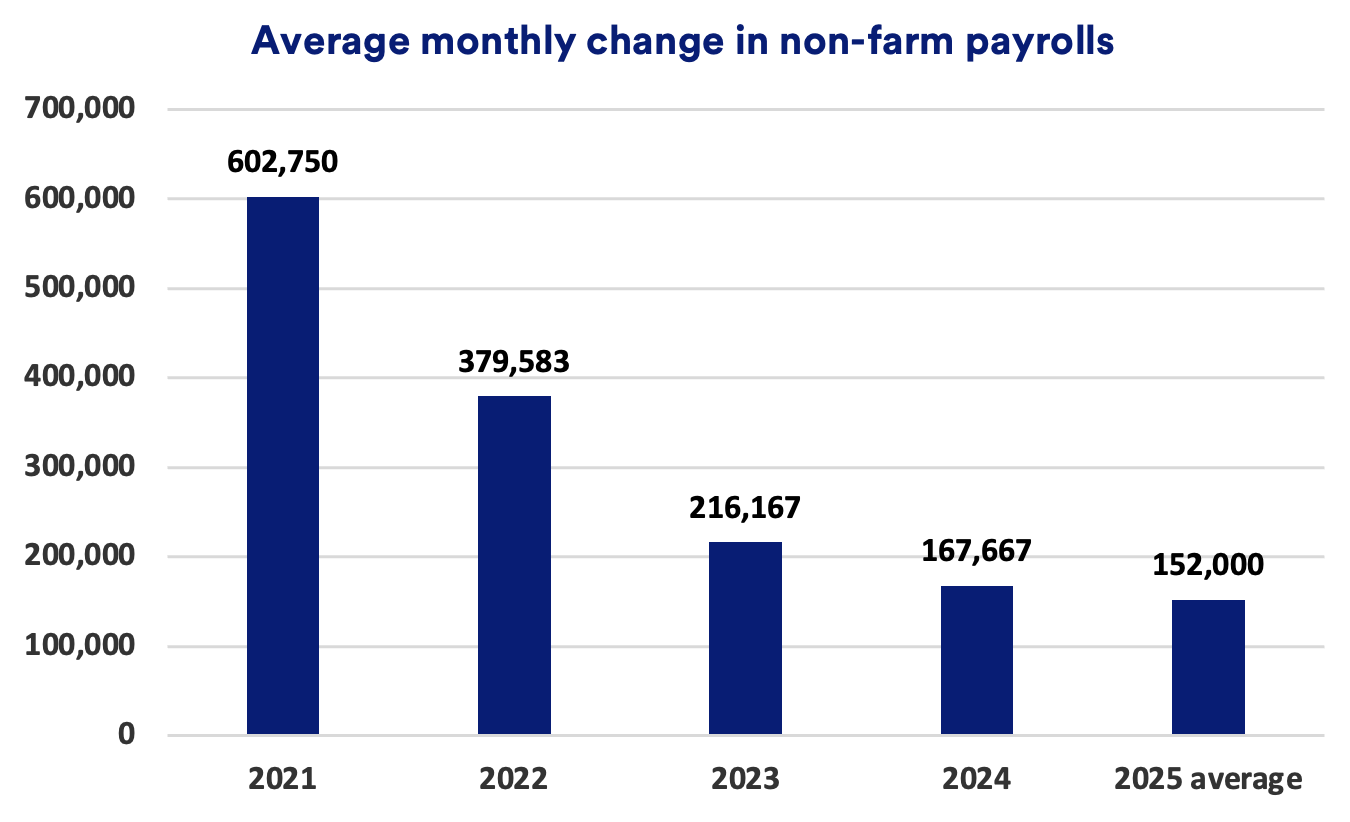

Job growth in the labor market picked up in March.

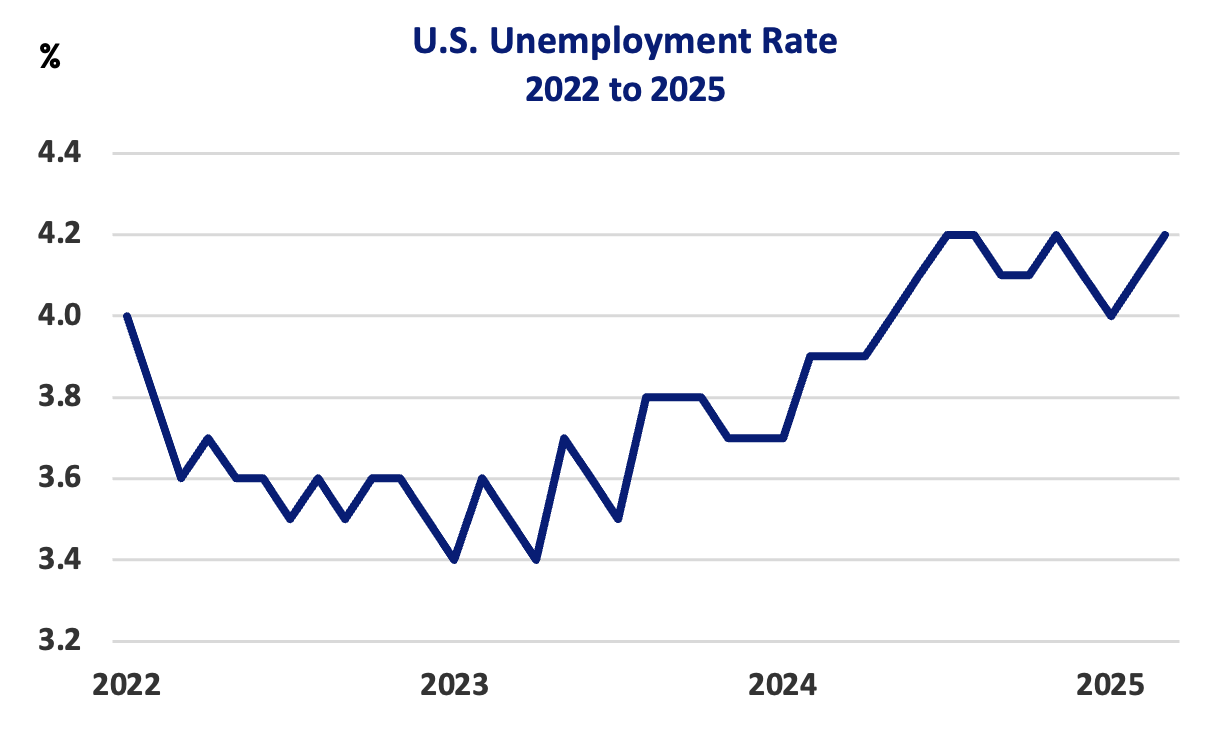

At the same time, the unemployment rate ticked up to 4.2%.

Investors want to know if the labor market’s continuing strength has staying power.

The labor market is maintaining momentum just as the U.S. economy confronts new challenges tied to the Trump Administration’s rollout of sweeping new tariffs. U.S. employers added as many jobs in March 2025 as in the two previous months combined, based on the latest U.S. Bureau of Labor Statistics data.1

“The labor market data we see is backward-looking,” says Rob Haworth, senior investment strategy director for U.S. Bank Asset Management. “Nevertheless, this report shows we’re keeping up with population growth, which requires at least 100,000 payroll jobs added per month. The latest report is constructive.”

As is frequently the case, the healthcare industry was responsible for the month’s biggest job gains, adding 54,000 positions.1 “Healthcare is an area where we’re chronically understaffed,” says Tom Hainlin, senior investment strategist with U.S. Bank Asset Management. “It is an industry with more than one million job openings, so there is more opportunity for continued growth, but employers can’t find enough workers.”

Other major contributors to February’s job gains included social assistance (+24,000 jobs in March), retail trade (+24,000), transportation and warehousing employment (+23,000). Federal government employment, a major focus of Trump administration cost-cutting measures, officially declined by 15,000 jobs between February and March.1

Trends in federal government jobs are an increasing focus. The Trump administration is seeking to trim the federal workforce. The numbers could drop further in the coming months. “Federal jobs are only a modest number in terms of total payrolls,” says Haworth. “However, there could be ripple effects, as by some estimates, there are two private contractors associated with every federal employee.”

The unemployment rate moved modestly higher, from 4.1% in February to 4.2% in March.1 “When taking a more historical view of the unemployment rate, a number in the low 4% range is quite favorable,” says Haworth.

Job openings data shows 7.6 million open positions as of the end of February 2025.2 As has been the case since 2020, the number of job openings outpaces the number of unemployed workers. “The Job Openings report indicates that employers are still looking to hire people,” says Haworth.

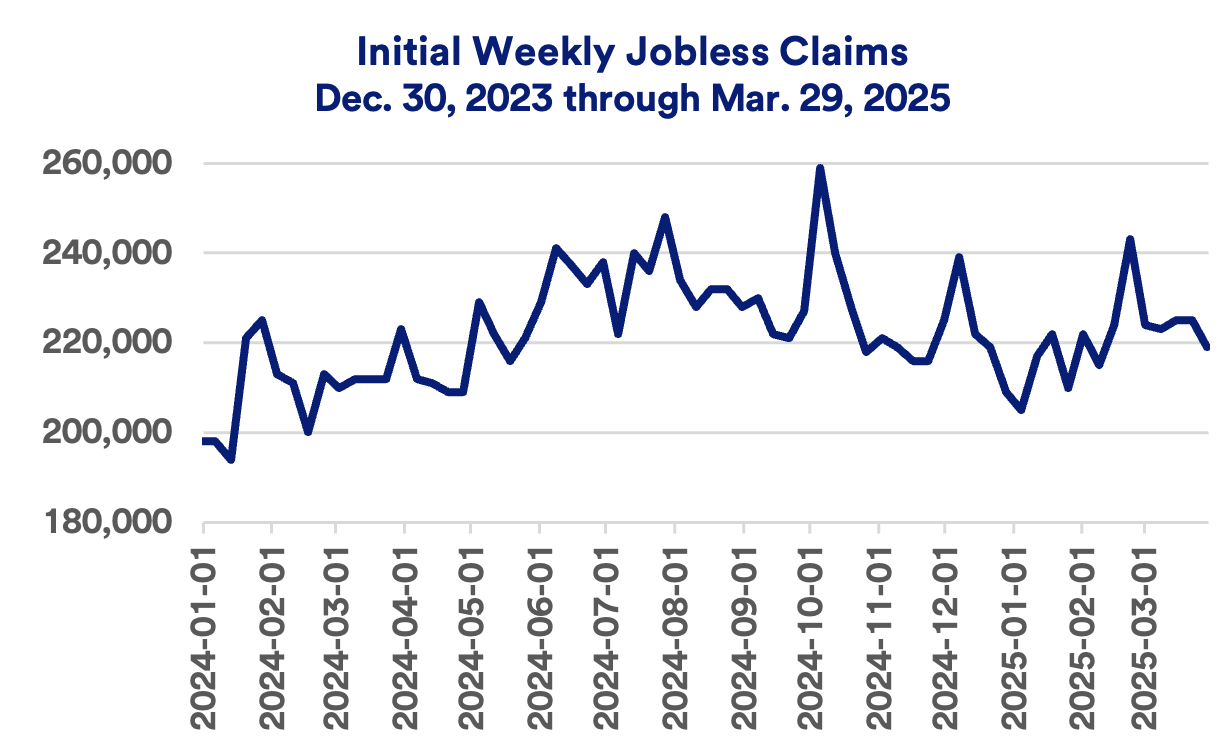

The closest thing to a “real-time” labor market measure is the weekly initial jobless claims report. This number often fluctuates from week-to-week. In late February, initial claims jumped to 243,000, raising some concern. However, claims dropped by the following week and remained relatively flat since.3 “One week’s numbers represent a data point, not a trend,” says Haworth. “If you look at long-term history, sub-300,000 initial weekly jobless claims are considered a fairly healthy level for the economy.”

Markets also track the labor force participation rate, considered a key barometer of the broader economy's health. This number hasn’t changed much over the past year, and stands at 62.5% based on March’s data.1 Throughout 2024 and early 2025, the labor force participation rate remained in a narrow range of 62.4% to 62.7%.4 “Improving labor participation is one way to address tightness in the labor market that’s propping up wage gains,” says Matt Schoeppner, a senior economist at U.S. Bank.

“When taking a more historical view of the unemployment rate, a number in the low 4% range is quite favorable."

Rob Haworth, senior investment strategy director, U.S. Bank Asset Management

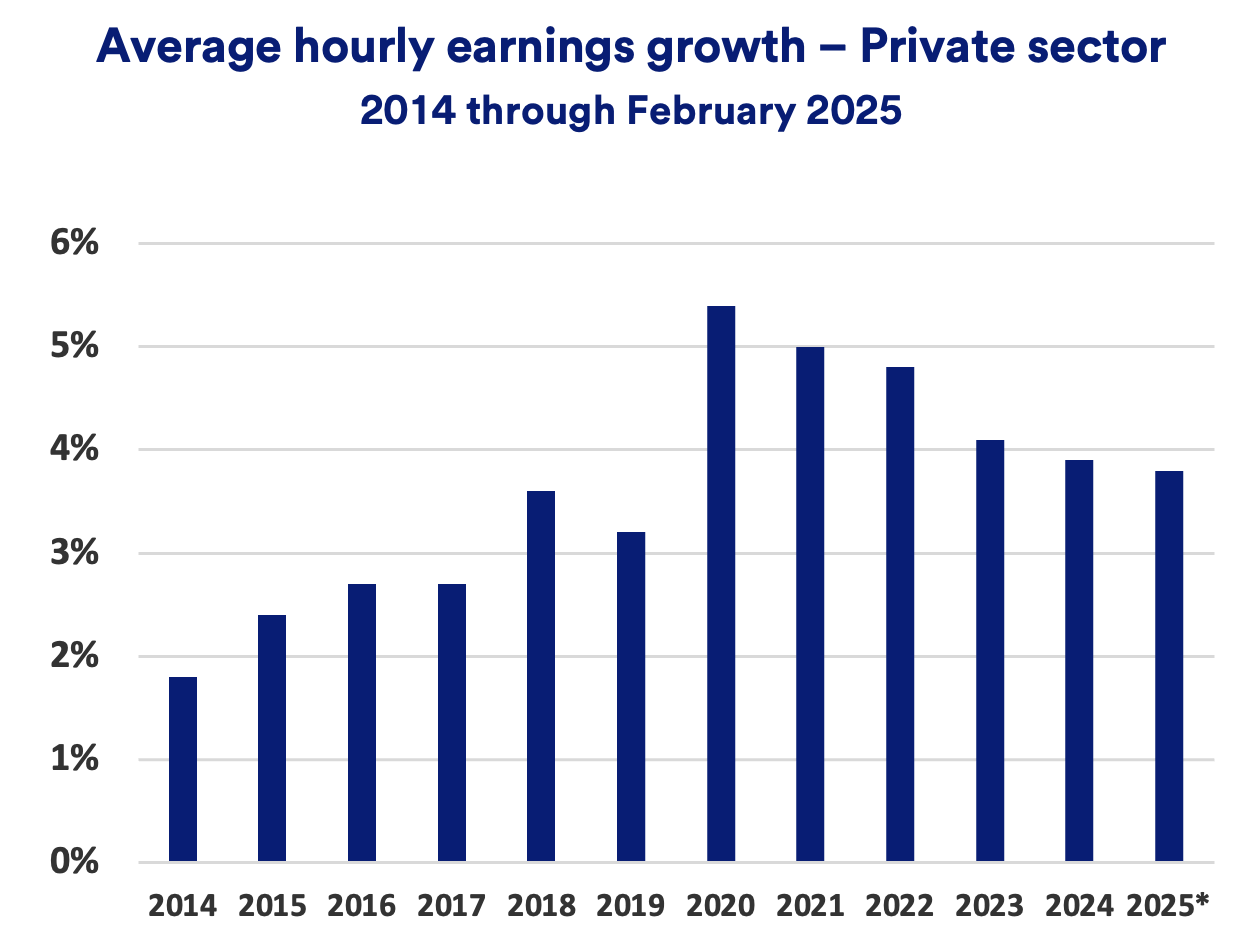

According to the March jobs report, average hourly earnings increased 3.8% over the past year, a slight decline from previous levels.1 Nevertheless, wage gains still exceed the inflation rate, as measured by the Consumer Price Index. Inflation for the 12 months ending in February measured 2.8%.4

Overshadowing the data are growing market fears of economic challenges ahead. In the two trading days following President Donald Trump’s April 2 announcement of significant new import tariffs, the S&P 500 declined nearly 10%. It re flects investor concerns over economic ramifications that could hinder the labor market.

Federal Reserve (Fed) chair Jerome Powell says the new trade environment creates a “highly uncertain outlook.” He noted the potential inflation threat from tariffs, saying, “Our obligation is to keep longer-term inflation expectations well anchored and to make certain that a one-time increase in the price level does not become an ongoing inflation problem.” Powell indicated the Fed would be in no hurry to further cut the federal funds target rate.5 In late 2024, the Fed cut rates by 1.0% but has not made any rate cuts since.

Investors closely track jobs data as an important economic indicator and a potential signal about Fed monetary policy. The latest jobs report reflects March’s employment environment. Along with the impact of tariffs on the labor market, Haworth is also monitoring the effects of tighter immigration policies proposed by the Trump administration. “People subject to deportation, in many cases, came to America to work, so if they leave, other workers will need to step into those jobs.” Haworth says the construction industry is a key area where the labor market may tighten.

Talk with a wealth professional if you have questions about your personal financial circumstances or investment portfolio.

The job market refers to the marketplace where individuals seek work and employers seek workers. The strength of the job market is considered one important measure of the current health of the broader economy. If more jobs are being created and demand for labor is high, it tends to reaffirm the presence of an expanding economy. By contrast, higher unemployment levels and low job growth (or a decline in job growth) indicate a slowing economy.

The unemployment rate, reported monthly by the U.S. Bureau of Labor Statistics, provides significant insight into the health of the nation’s economy. Generally, the lower the unemployment rate, the stronger the economy is likely to be. The unemployment rate is also one of the mostly closely followed indicators. It’s important to note that the unemployment rate reflects people who are out of work but still seeking employment. It does not reflect others who have stopped looking for work or consider themselves no longer in the labor force.

When the unemployment rate moves higher, it indicates potential weakening of the economy. Consumers may consider holding back on purchases if they have concerns that they, themselves, could face unemployment soon. If that occurs, it can potentially contribute to further economic weakness. When unemployment is low, it’s a good indicator that the economy is strong and expanding.

1 U.S. Bureau of Labor Statistics, “Employment Situation Summary, March 2025,” April 4, 2025.

2 U.S. Bureau of Labor Statistics, “Job Openings and Labor Turnover Summary, February 2025,” April 4, 2025;

3 U.S. Department of Labor, Employment and Training Administration.

4 Source: U.S. Bureau of Labor Statistics.

5 Cox, Jeff, “Powell sees tariffs raising inflation and says Fed will wait before further rate moves,” CNBC.com, April 4, 2025.

After two years of solid growth, how is the economy setup to perform in 2025?

We can partner with you to design an investment strategy that aligns with your goals and is able to weather all types of market cycles.