IRA vs. 401(k): What's the difference?

Year end tax planning tips

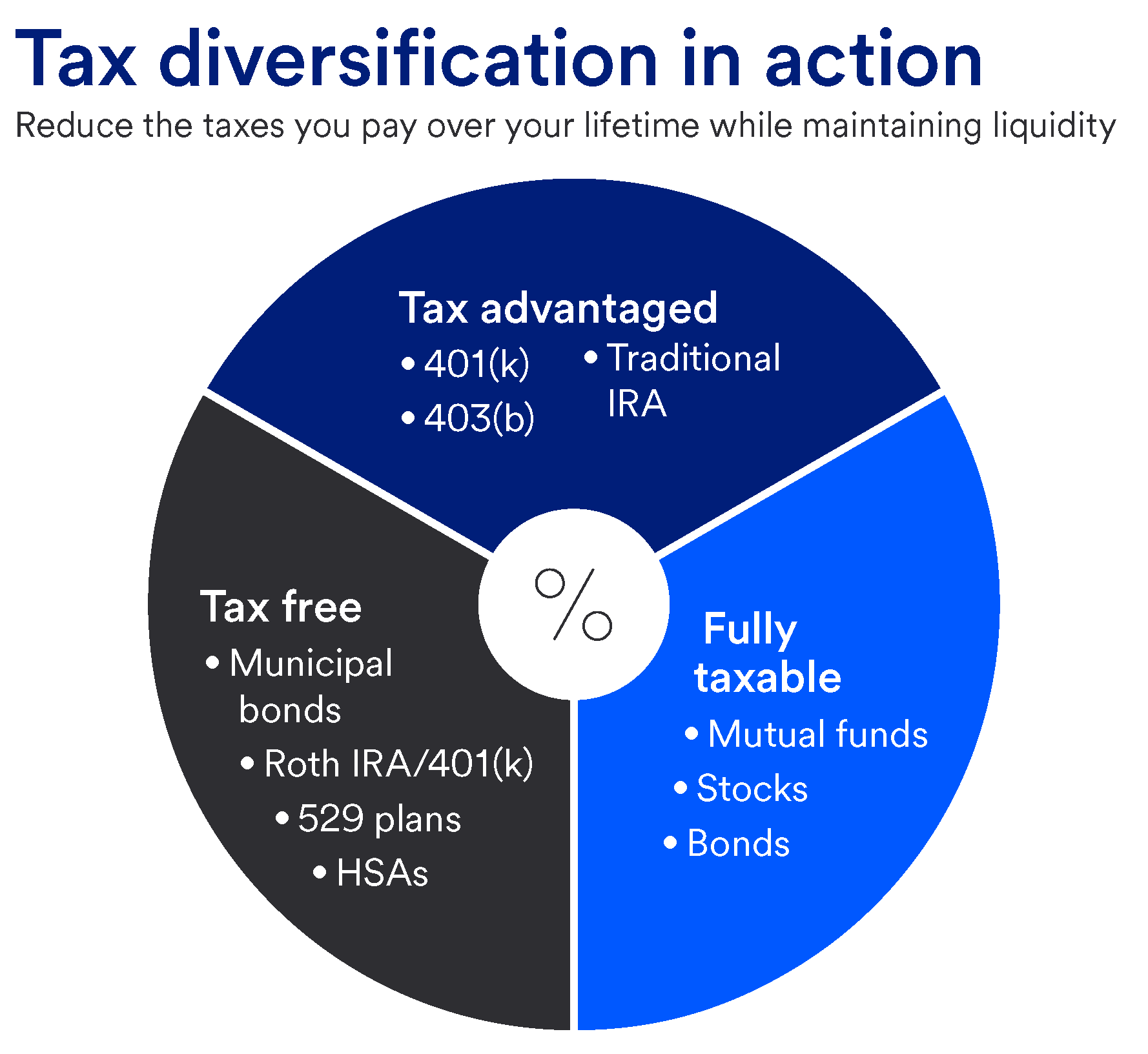

![]()

You know it’s important to diversify your investments across stocks and bonds to potentially reduce risk. But did you know you can also diversify your investments for more tax-efficient investing?

Tax diversification is an investment strategy that considers the tax treatment of specific assets and accounts. The goal of tax diversification is to reduce your long-term tax burden while giving the liquidity you need for short-term expenses.

Some investment accounts are subject to annual taxes whenever you receive income from them but allow you to make penalty-free withdrawals when you need immediate access to cash. Other accounts defer your taxation until retirement – or allow you to make tax-free distributions – but may have restrictions on when you can access your money.

Understanding which accounts fit into each category can help you build a tax-diversified portfolio that best meets your needs, both today and years down the road.

Retirement accounts such as 401(k)s, 403(b)s and traditional IRAs are considered tax-advantaged investment accounts (also called tax-deferred investment accounts).

Traditional retirement accounts like a 401(k) or 403(b) are popular, as they’re often an employer-offered benefit. Many employers even match contributions up to a certain amount. If you don’t have access to an employer sponsored plan, a traditional IRA provides similar tax benefits (although there are different contribution limits).

These types of retirement accounts can help reduce your taxable income today but, due to RMDs, can also move you into a higher tax bracket in retirement.

A traditional brokerage account (generally comprised of stocks and bonds) is fully taxable.

While a traditional brokerage account doesn’t offer tax benefits, it’s the most flexible in terms of withdrawals. It’s a good addition to your portfolio if you’ve maxed out contributions to your retirement accounts and want to continue investing.

Roth IRAs and Roth 401(k)s, municipal bonds, 529 savings plans and health savings accounts (HSAs) are considered tax-free investment accounts.

Tax-free assets and accounts like health savings accounts and municipal bonds help limit your tax liability whenever you make a withdrawal. Roth accounts, on the other hand, are most beneficial as you near retirement.

Since the withdrawal of earnings from a Roth 401(k) or Roth IRA is generally tax-free after age 59½, you could end up paying less income tax in your later years.

Tax diversification makes use of a variety of investment accounts with different tax treatments: fully taxable, tax-advantaged, and tax-free. Below are three strategic approaches that can help you lower your taxes now and be tax-diversified in retirement.

Both traditional (tax-advantaged) and Roth (tax-free) accounts help reduce your overall tax burden, allowing you to keep more of what you earn. Putting some of your savings into each of these tax buckets can provide an even bigger benefit.

When you reach age 59½, consider withdrawing just enough from your tax-advantaged accounts to keep you in a lower tax bracket and then tap your tax-free Roth accounts for any remaining needs.

Investing evenly between tax-advantaged and tax-free accounts is a good way to diversify for some retirement savers. But if you’re earlier in your working life and expect your income to increase in future years, you may want to prioritize Roth accounts. Your contributions will be taxed at the lower rate you’re paying today, but you’ll have the opportunity to access that money, tax-free, when you retire.

If you have already reached your peak-earning years, however, you may want to shift toward traditional accounts that allow you to make pre-tax contributions.

Fully taxable investments, including interest-bearing bank accounts and brokerage accounts, can play an important role in your portfolio. While they don’t enjoy the same long-term tax benefits that retirement accounts offer, the ability to tap these funds at any time without penalty can be valuable.

When it comes to lowering your taxes over a lifetime, awareness is key. Understanding when and how to choose the right investment account for your goals and life stage can help you minimize your tax bill and maximize your income in retirement. A financial professional can help ensure your investment strategy is optimized in a tax-efficient manner reflective of your needs.

Learn how we can work with you to create a wealth and investment plan customized to your financial goals.

Related content