How much money do I need to start investing?

Guide to personal loans: 7 questions to ask

For lenders short on loan servicing expertise, outsourcing helps ensure the work gets done without the in-house headaches.

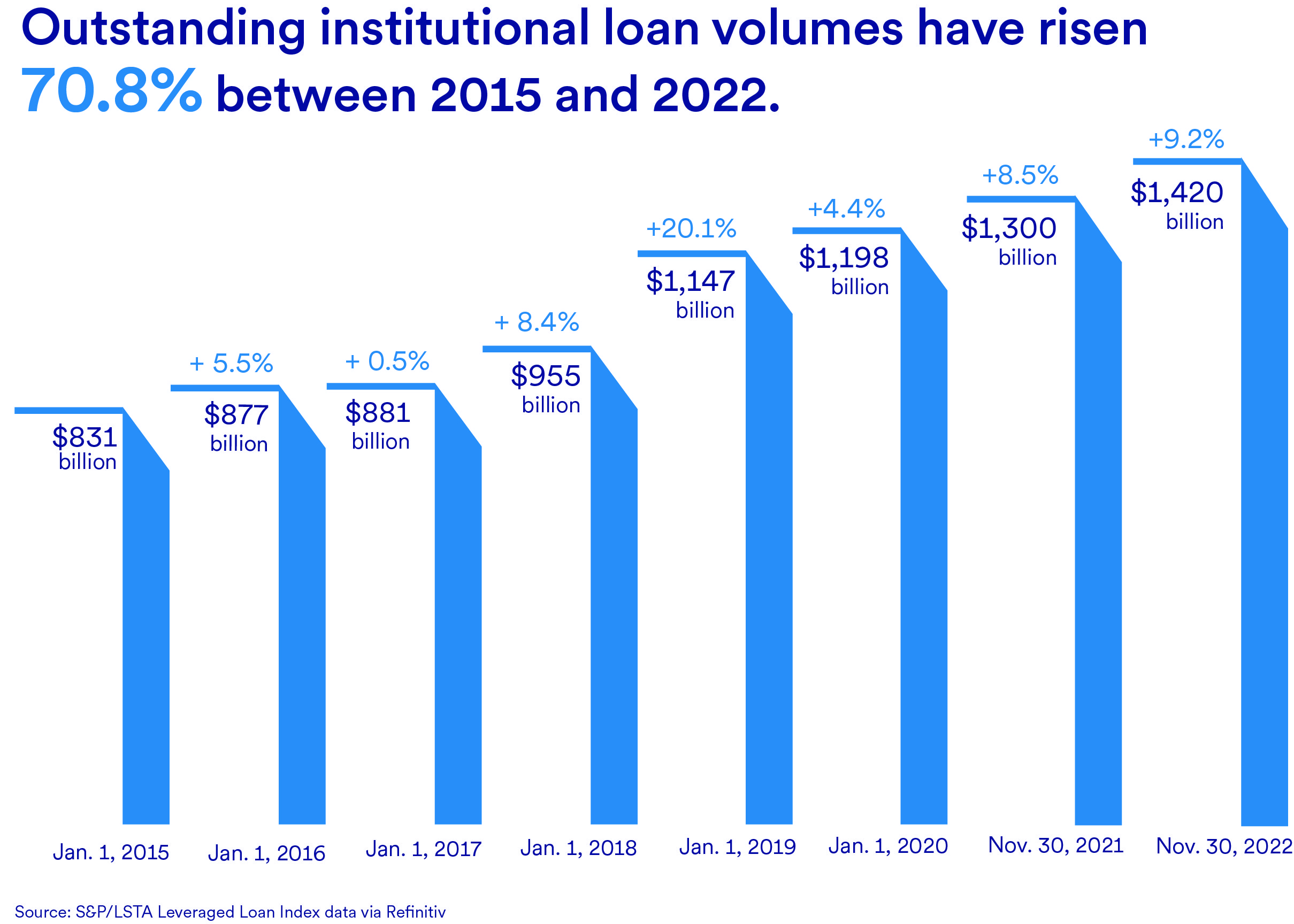

Aside from a lull in the aftermath of the Great Recession, the leveraged loan industry has grown steadily over the past 20 years with outstanding loan volumes topping $1.42 trillion in the fourth quarter, according to Refinitiv.

Given the industry’s expansion and increased regulation on the traditional banking sector, a number of new non-bank lenders have entered the field. However, many newcomers have struggled to manage all that’s required after a loan closes.

The complexities of lending

“Administrative tasks associated with loan servicing can often shift a lender’s focus away from what they do best – credit monitoring,” says Jim Hanley, vice president at U.S. Bank Global Corporate Trust.

Meanwhile, as investors contend with consistently low interest rates, the market wide search for better yields has led to some tangled loan structures for nontraditional lenders.

To ease such headaches, many loan providers – especially those of the nonbank variety – are turning to third parties to take on a host of loan agency services.

“Many loan providers – especially those of the nonbank variety – are turning to third parties to take on a host of loan agency services.”

“We’ve been brought in by large lending firms that have been syndicating loans to other funds. They realize they need to lower their risk profile as well as streamline some of their back-office responsibilities so they can concentrate on other things,” Hanley says.

Servicing a key element of the loan landscape

For many in the leveraged loan industry, the enticing part of the business is origination. What’s done afterward, however, could make the difference later between a repeat customer and a disgruntled borrower.

From processing the transaction through administering collections and payments – and handling all communications throughout – it’s critical to smooth out the inevitable bumps.

Yet, related expenses can add up. According to the Loan Syndications and Trading Association (LSTA), loan service costs are tied to:

“Plus, there are a limited number of experts in the field. So, finding them, hiring them and training them takes a lot of time and manager bandwidth that could otherwise be focused on growing the firm’s business,” Hanley says.

As for lenders wary of handing off a hard-won customer to another financial entity, a quality outsourcing partner will offer a customizable solution that allows the lender’s identity to remain front and center.

“Some firms want to keep it in-house because they value the many touchpoints this model brings to the lending relationship,” says Michael Zak, senior vice president and business development officer at U.S. Bank Global Corporate Trust. “In a white-label solution, the lender is still the administrative agent and retains the same relationship touchpoints. The operational mechanics just shift to a third party that does the heavy lifting behind the scenes.”

An adept third-party partner adds value

Since the Great Recession ended, a host of bank regulations have been enacted to better protect borrowers. As a result, many large banks have reduced their exposure to the loan servicing industry, opening the door for many smaller entities to enter the field.

While the competition has sparked innovation and responsiveness within the space, a number of key considerations have remained constant, including:

“Many non-bank lenders are very cost-conscious, and they don’t want to hire a staff of 10 people or more to handle all of these back-office duties,” Zak says. “So, it makes sense to outsource the role to process the operational items that they don’t want to deal with.”

Partnering with a sound financial institution

As you weigh your third-party options, look for a partner that’s dedicated to following the rules and regulations around loan agency services.

“There’s a built-in trust factor because we, as the highest rated bank by the rating agencies, have significant scale and follow a sound operational and risk profile,” says Matt Clarkin, CFA and vice president in product management with U.S. Bank Global Corporate Trust. “Many non-bank lenders that don’t have their own internal capabilities find U.S. Bank to be a natural partner.”

Clarkin added that U.S. Bank offers its customers a number of benefits including:

“At U.S. Bank, we offer true plug-and-play solutions, so customers don’t have to find and hire experienced people,” Hanley says. “And going forward, we can scale up with them as they grow.”

U.S. Bank has a sound financial history and extensive expertise in servicing loans. To learn more about our loan agency services, visit usbank.com/corporatetrust.

Related Content